The home lending market in 2022 was characterized by extreme fluctuations, and 2023 might witness more of the same. This survey paints a picture of a challenging landscape in 2022 for borrowers, renters, and lenders, largely due to high-interest rates and the possibility of an economic downturn.

Several notable highlights of the survey:

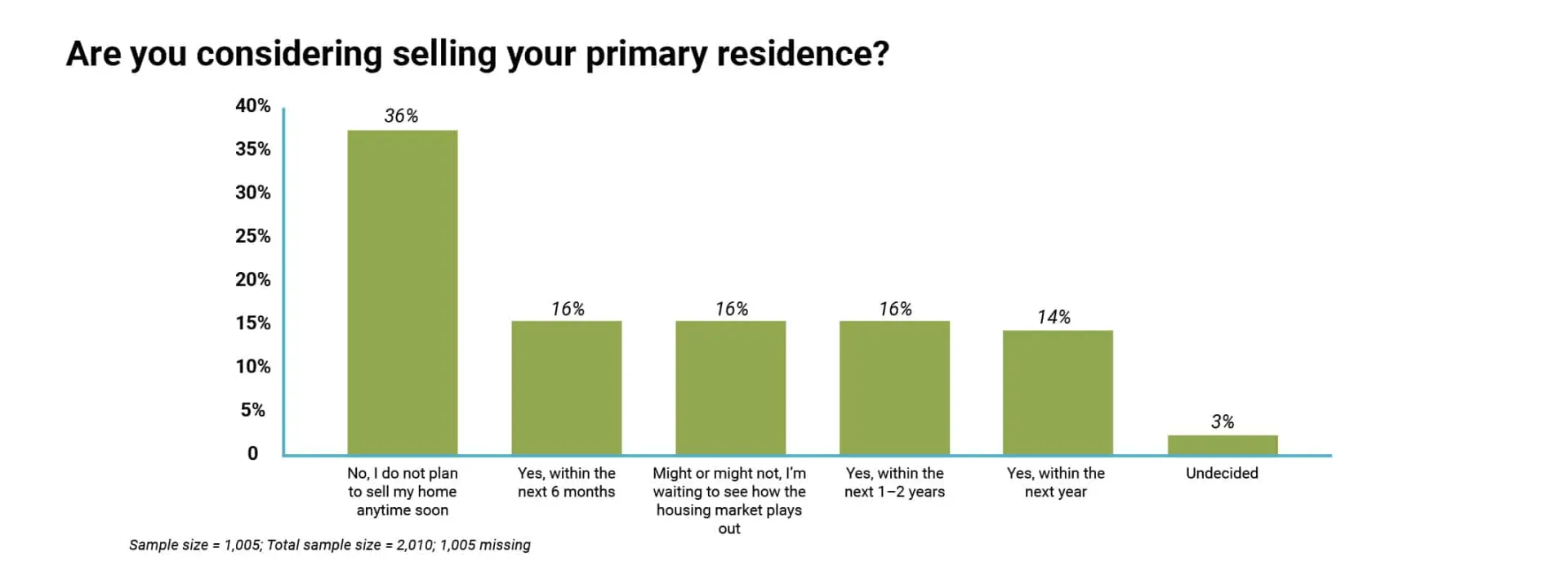

- 36% of current borrowers intend to stay in their present homes, while 16% are uncertain about seeking new housing.

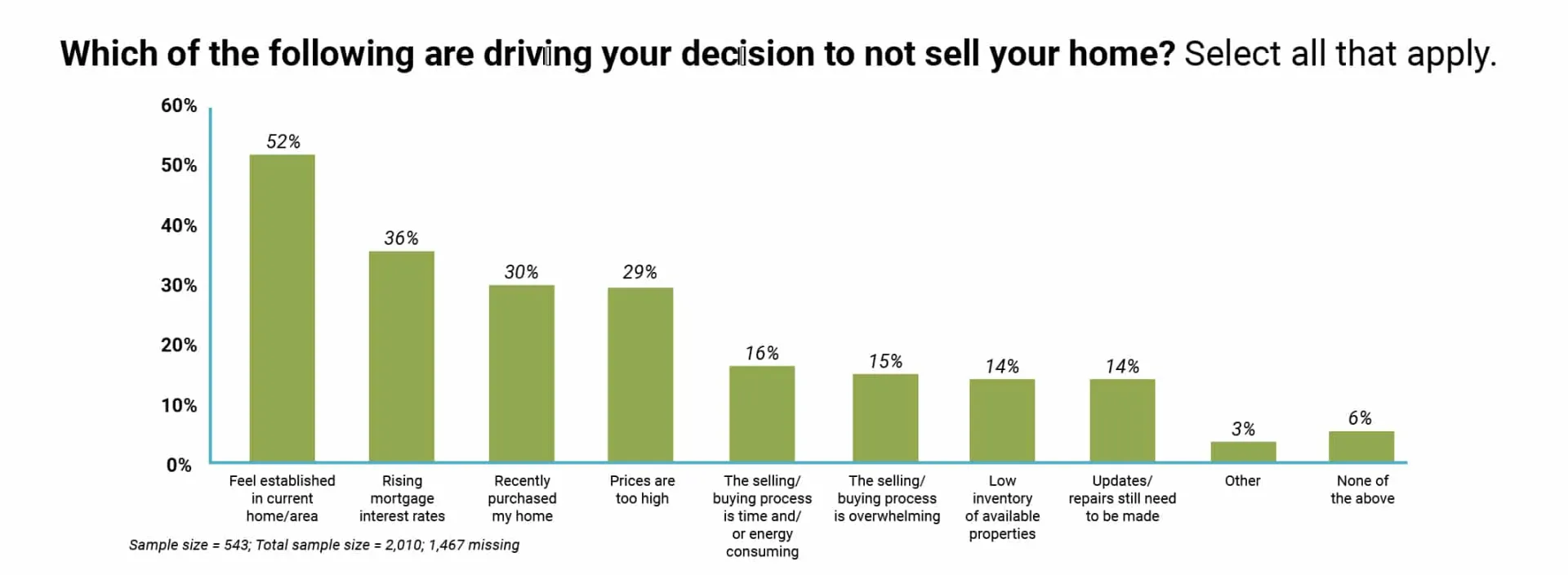

- Among those who have decided to stay put, 36% attribute their decision to high-interest rates.

- 34% of current renters in the sample were once homeowners.

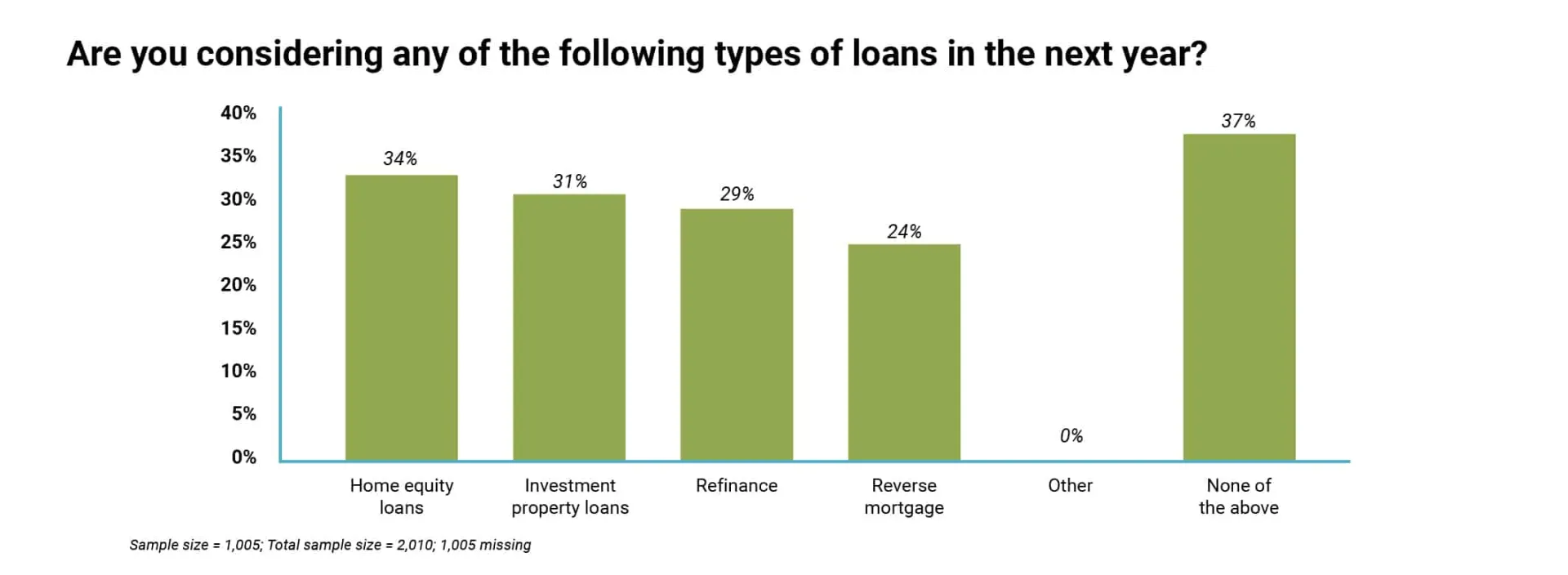

- 63% of recent borrowers plan to look for new financing, considering options like home equity loans, reverse mortgages, refinancing, and investment property loans.

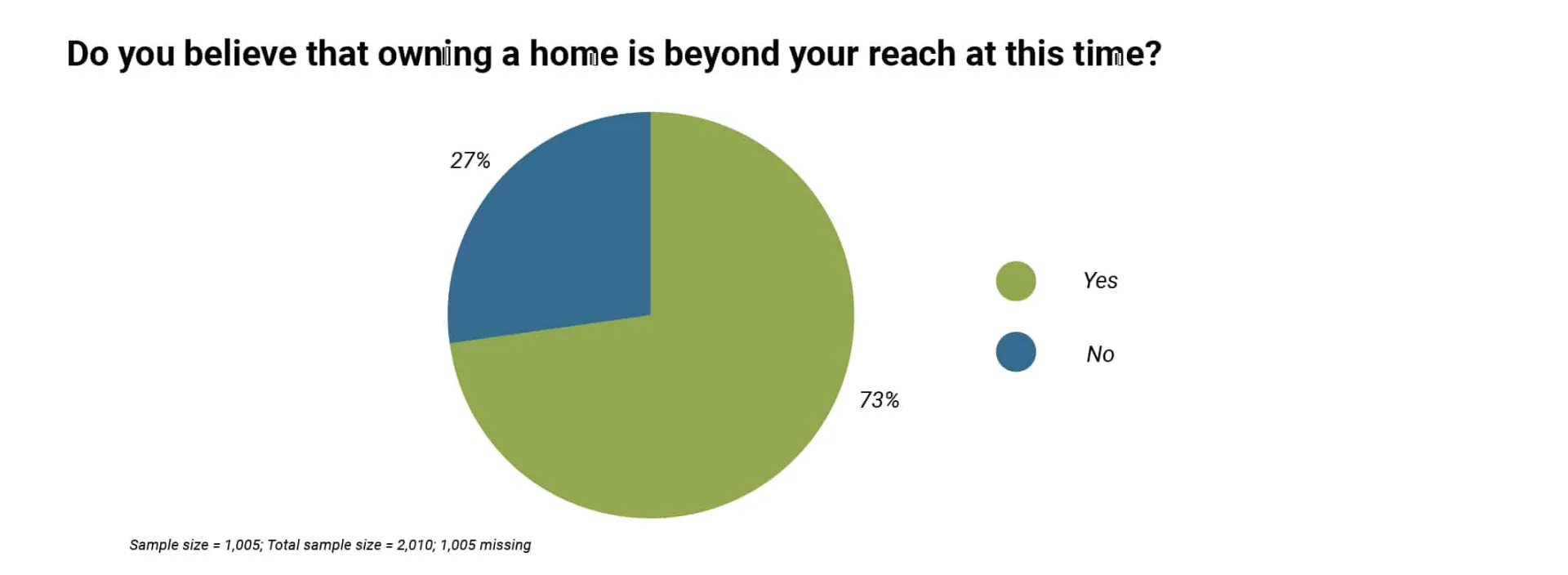

- 73% of renters believe homeownership is currently out of their reach.

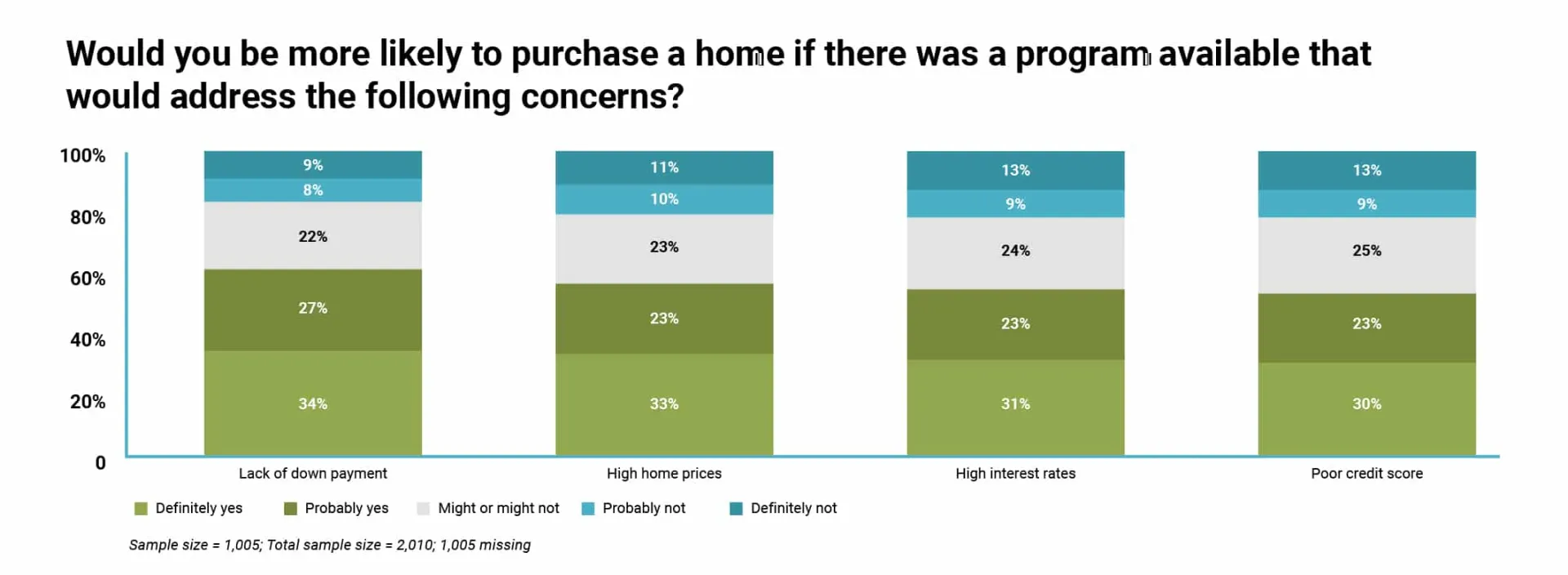

- 56% of renters would be more likely to buy a home if a program addressed high home prices, and 54% would be more likely to purchase if a program tackled high-interest rates.

Predicting whether 2023 will see improvements remains uncertain. While the future is unknown, it’s clear that winning every borrower is more critical now than ever. Establishing new borrower relationships and deepening existing ones is always crucial. But what exactly do borrowers want and need?

Sprint Funding aims to help you answer that question by offering insights from the survey regarding borrowers’ priorities and preferences.

According to the survey, borrowers are looking for:

Flexibility

53% of respondents consider flexible loan options as one of the most critical aspects of mortgage financing.

Savings

67% view saving money as one of their top three concerns when financing a mortgage, with 56% citing low lender fees.

Education and guidance

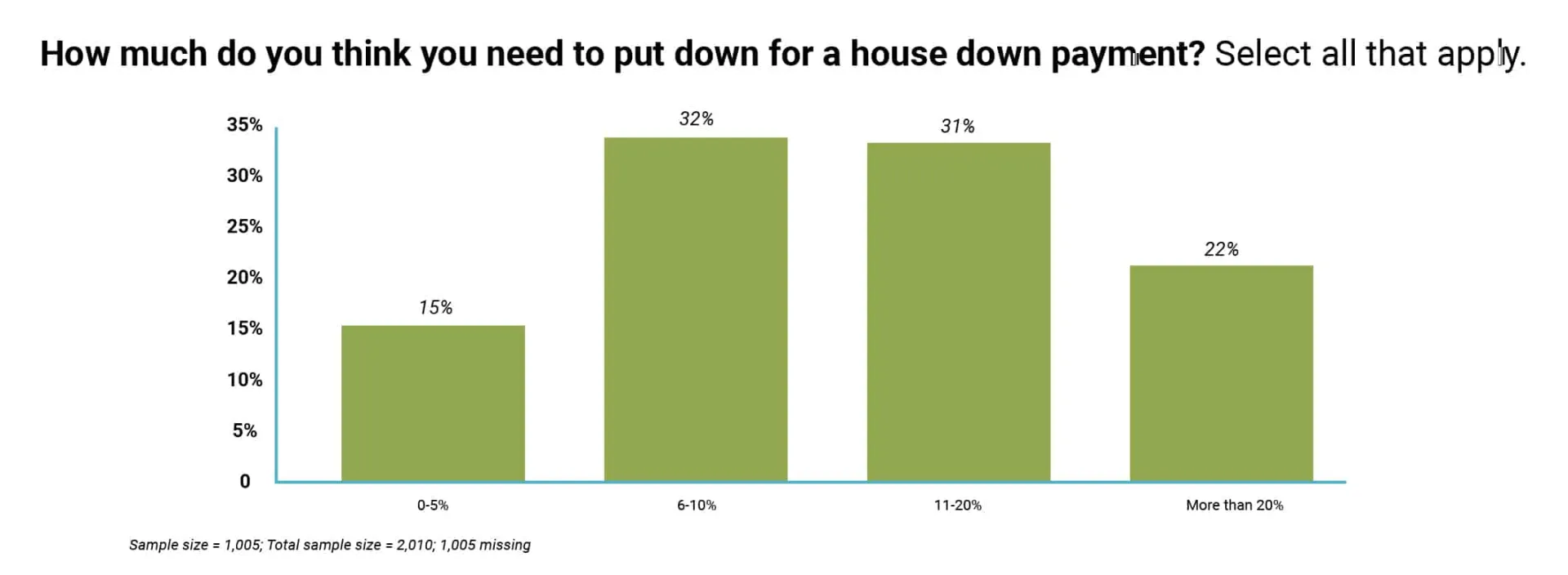

Many renters still perceive homeownership as more challenging than it is, with 53% believing they need to provide more than a 10% down payment.

High tech and high touch

Only 9% of borrowers desire a fully digital experience, although many appreciate the convenience of digital processes and services.

Varied outreach based on different experiences

Experienced borrowers (those who have taken out five or more mortgages in their lifetime) prefer digital offerings, while those who purchased during low-interest rate periods (one to two years ago) are most likely to be cautious about selling their homes.

Trusted referrals

Inexperienced borrowers rely on referrals from realtors, family, or friends to choose lenders.

2023 Insights: Borrower Preferences in Unpredictable Times

Overview: Navigating a volatile year for borrowers and renters.

The 2023 Borrower Insights Survey depicts borrowers and renters grappling with an uncertain landscape. Despite the challenges, certain aspects remain constant.

The market continues to welcome new borrowers, and both borrowers and renters consistently seek more space, better value, and the financial advantages and increased security associated with homeownership.

Around 46% of borrowers who took out a mortgage in the past five years have only had one or two mortgages in their lifetime, including both home purchases and refinancing.

Nearly two-thirds of recent borrowers (63%) plan to explore new financing options such as home equity loans, reverse mortgages, refinancing, or investment property loans.

Over a third (34%) of current homeowners who obtained a mortgage within the last five years intend to take out a home equity loan in the coming year.

Refinancing is being considered by 29%, potentially reflecting interest rate fluctuations. Additionally, 24% are mulling over a reverse mortgage.

Meanwhile, 31% are thinking about investment property loans, suggesting some confidence in increasing home values.

More than a third of borrowers are likely to remain in their current homes.

Thirty-six percent of respondents don’t have any immediate plans to sell their homes. An extra 16% are uncertain about selling, as they’re keeping an eye on how the housing market unfolds. Meanwhile, 3% are undecided.

Renters’ Perspectives on Homeownership

Over a third of current renters have a history of homeownership.

Thirty-four percent of individuals currently renting revealed that they had previously participated in home buying or refinancing processes. It’s possible that they were priced out of the market or encountered financial setbacks, causing them to transition from homeownership to renting.

The majority of renters believe homeownership is out of reach.

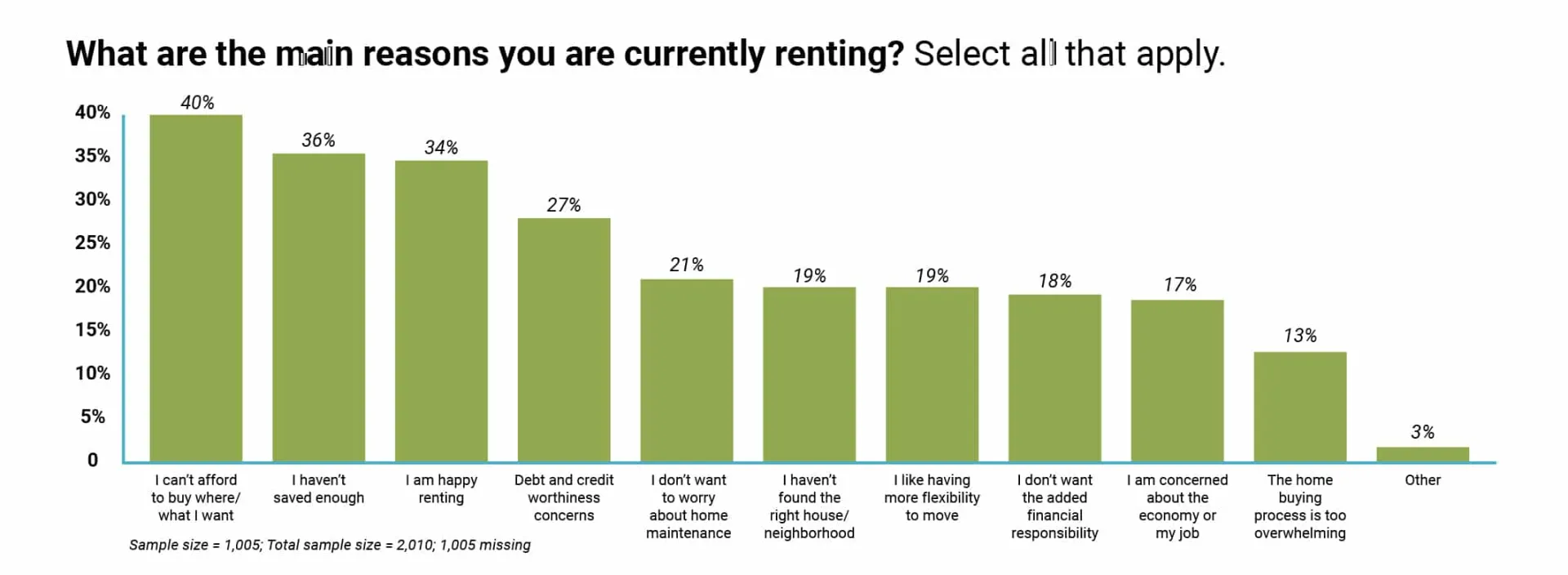

Insufficient funds were cited as the main reason for renting, with 73% of renters thinking they couldn’t afford a home at the moment.

Economic factors were specifically mentioned by more than half of the respondents.

Fifty-six percent of current renters claimed they would be more inclined to buy a home if a program addressed high housing prices.

Similarly, 54% stated they would be more likely to purchase if a program tackled high-interest rates.

Renters’ Challenges and Motivations for Homeownership

Other factors influencing the decision to rent include not being able to afford the desired location or property type (40%) and insufficient savings (36%).

Although borrowers are seeking more space and attractive deals, fewer are trying to transition from renting to buying, possibly indicating the difficulty of such a move in the current climate. Current homeowners who recently participated in the mortgage process cited “more space” and “finding a good deal on a house” as their primary reasons for buying a home (41% each).

This is a shift from 2022 when “not wanting to rent anymore” (38%) was mentioned more frequently than finding a good deal (36%) or needing more space (36%).

The year-over-year change may suggest that transitioning from renting to homeownership has become more challenging in the current environment.

Forty-six percent of respondents plan to sell their homes within two years or less, with the most common reasons being to capitalize on increased home equity/value (39%), change scenery (38%), or to downsize or upsize (36%). Despite obstacles, renters appear driven to purchase properties.

Renters demonstrate a willingness to make significant efforts to buy a home, even considering relocation to another state if it means they could afford a house (56%).

What factors could persuade them to buy instead of rent?

Some are searching for the right deal or aiming to save; 49% of renters would buy a home if they found a good deal, and 41% would if they had saved enough money.

As expected, generational differences exist among the sample, showing a positive indication. Younger borrowers and renters seem poised to invigorate the market. These groups differ from previous generations in ways that appear promising for the future of the home-buying market.

Younger borrowers appeared more active and significantly more likely to plan on selling within the next two years.

Sixty-five percent of Gen Z and Millennial homeowners intended to sell during that period, in contrast to twenty-six percent of Gen X and older individuals.

This trend may be attributed to younger borrowers finding their financial footing and adopting an expansion-oriented mindset. They were more likely to buy a house because they had saved enough money (44% versus 25% of Gen X and older).

Older borrowers (Gen X and older) took a more conservative approach, pointing to “not wanting to rent anymore” as their reason for purchasing a home (42% versus 33%, respectively).

Younger borrowers are transitioning into homeownership as they establish their lives and attain greater financial stability. Meanwhile, older borrowers seem driven by the financial benefits of homeownership.

Among renters, Gen Z was the most optimistic group, with 37% believing that homeownership was within their reach (compared to 27% overall).

Moreover, two-thirds of Gen Z and Millennial renters expressed a willingness to relocate (67%) as a means to achieve homeownership, in contrast to a mere 48% of Gen X and older individuals.

Borrowers’ Preferences When Choosing a Lender

In the face of economic turbulence, both borrowers and renters will require more guidance. Lenders can offer assistance in ways that foster long-lasting relationships. But apart from their financial concerns, what are active and prospective borrowers seeking?

The survey offers valuable insights into their preferences, which include:

- Flexibility – Providing financial flexibility can help borrowers bridge the affordability gap. Fifty-three percent of borrowers surveyed considered the availability of flexible loan options as one of their most crucial factors when financing their mortgage. Flexible down payment options were cited by 49% of respondents. Flexibility was particularly important to Millennials, with 85% of them highlighting flexible down payment or loan options as vital, compared to 71% of Baby Boomers.

- Savings – Lower interest rates and costs are essential, especially for older borrowers, but younger borrowers also value loan options. Saving money is a top priority. Two-thirds of the survey participants (67%) stated that overall savings were among their top three concerns when financing a mortgage. The next most critical concern was low lender fees (56%).

In selecting a lender, Baby Boomers prioritized low interest rates. Younger generations, on the other hand, focused more on finding various loan terms and product options. As mentioned earlier, interest rates are especially important to Baby Boomers, while other generations have different priorities.

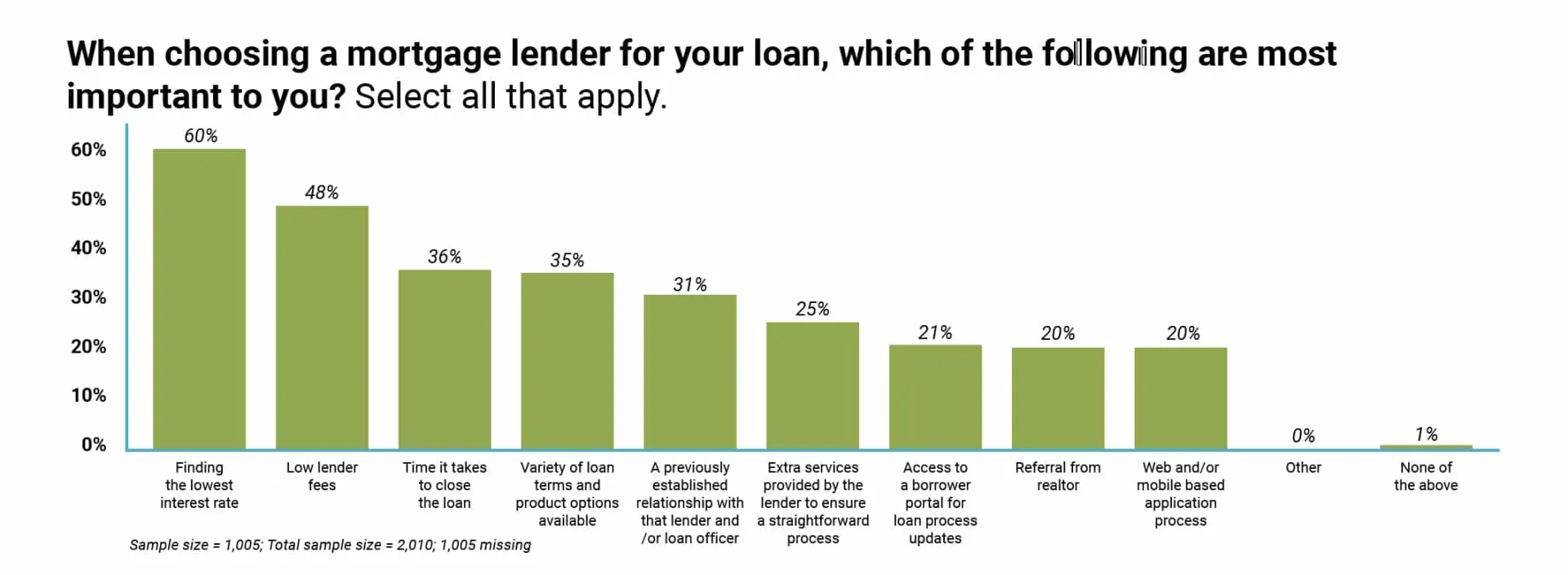

In 2023, the primary factor that borrowers considered when selecting a lender was the lowest interest rate (60%), followed by low lender fees (48%), and the time it took to close the loan (36%).

Older borrowers, particularly Baby Boomers, placed the most importance on low interest rates, with 90% of them considering it a top factor compared to only 42% of Millennials and Gen Z.

Younger borrowers, such as Gen Z and Millennials, were less concerned with savings and more interested in having a variety of loan terms and product options available to them (39% versus 31%).

When discussing their recent mortgage lender experiences, borrowers were most likely to mention receiving the best rate. The majority of respondents (90%) were satisfied with their latest lender, who met their expectations. A good lending experience was characterized by obtaining the best rate (60%) and having a seamless process from start to finish (60%).

These satisfaction metrics have increased since 2022, when 56% of respondents found the process easy and 55% felt they received the best rate. In summary, lenders are performing well in terms of rates and ease of use.

Borrowers also emphasized the importance of lower costs in the lending process. Reflecting on past experiences, they identified cost and communication as crucial factors. Fifty-five percent considered lower overall costs as one of the top three factors, followed by good communication and follow-up (50%), and lender transparency (40%).

In 2023, providing education and guidance to help borrowers comprehend the available options, such as credit and purchase programs, has proven to be beneficial in opening new opportunities. There is a growing need for more education and resources to help transform renters into homeowners.

A consistent finding from past surveys remains relevant – renters tend to significantly overestimate the challenges of buying a home. In fact, 73% of renters believe that homeownership is currently unattainable for them. Additionally, 53% of renters think that a down payment of more than 10% is required when purchasing a home.

In 2023, lenders have an opportunity to assist renters in overcoming their challenges. Six out of ten renters said they would be more likely to buy a home if a program could address their down payment difficulties (61%).

Similarly, most renters believed they needed at least a “good” credit score (700-749) to qualify for a mortgage (29%), but almost the same percentage thought they required a “fair” (650-699) or “very good” (750-799) credit score (25% each). Fifty-three percent mentioned they would be more likely to purchase a home if programs catered to their concerns about poor credit scores.

Borrowers desire a balance between high-tech and high-touch experiences. They tend to prefer traditional lenders over online alternatives. Understanding when borrowers want online tools versus in-person interactions is essential for establishing relationships and meeting them where they are.

Borrowers strongly favored traditional lenders, with fewer than one in ten wanting a fully digital experience (9%). They still sought in-person interactions, with 30% using a bank for their mortgage and 26% employing a mortgage broker. These numbers have remained consistent since 2022 (31% and 25%, respectively).

More experienced borrowers were slightly more inclined to use online services, with one in five homebuyers (who have taken out at least five mortgages) reporting that they utilized an online platform for their mortgage (19%).

The most sought-after experience combined high-tech and high-touch elements. Twenty-six percent of borrowers wanted an equal blend of traditional methods and digital tools for their next mortgage experience. However, the human touch held a slight edge, with almost the same percentage preferring only traditional methods (25%).

Borrowers were receptive to digital experiences, particularly those that simplify and streamline the loan process. A combination of high-tech and high-touch experiences is the norm in the home lending industry. For example, most borrowers closed their most recent loan by signing documents online and notarizing the remainder in person (35%). An additional 25% signed all documents online with a remote notary, with only 25% going to a title office with a notary.

This marks a slight shift from 2022, when the top three methods for closing loans were signing documents online and notarizing in person (30%), going to a title office with a notary (28%), and signing documents online with a remote notary (21%). In other words, high-tech and high-touch closings are increasingly gaining popularity.

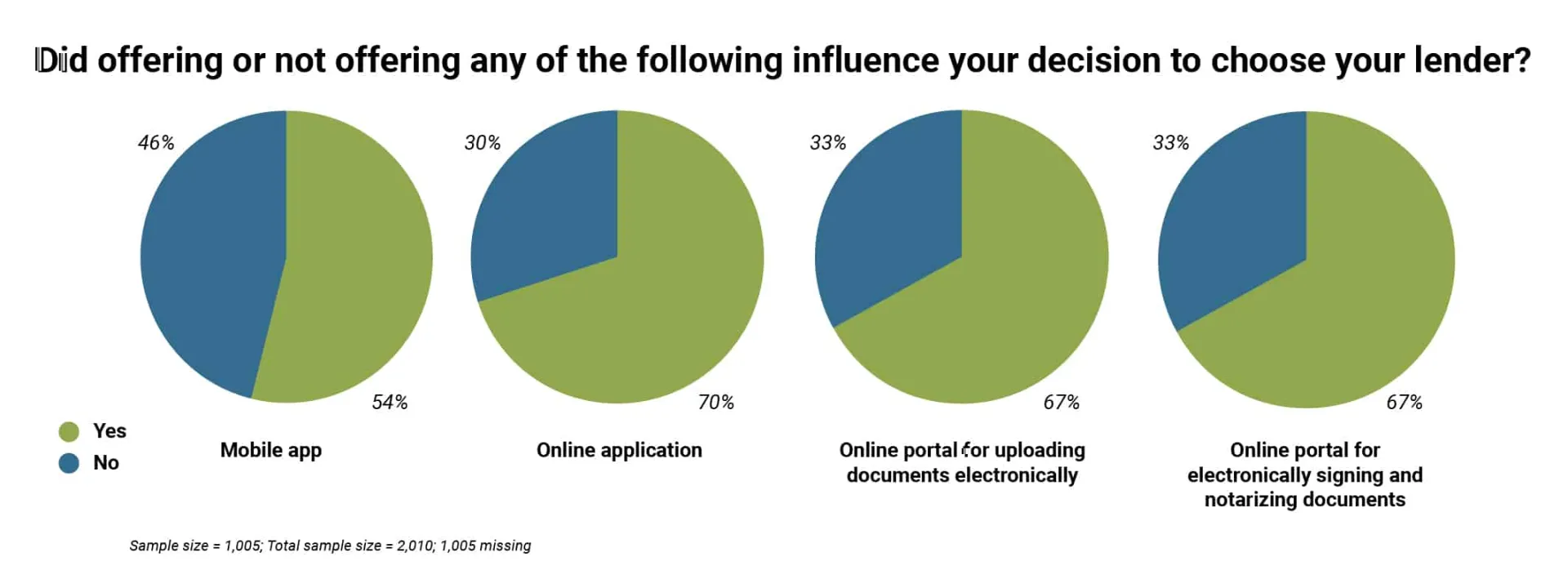

Seven out of ten borrowers claimed that being offered an online application influenced their decision to work with a specific lender (70%), up from six in ten in 2022 (60%).

Online portals are also in demand, with a growing number of borrowers being swayed in their choice of lender by the option of uploading documents through an online portal (67%, up from 59% in 2022) and using an online portal to sign and notarize documents (67%, up from 60% in 2022).

Younger borrowers preferred mobile apps, with 73% of Gen Z and Millennial borrowers stating that being offered a mobile app influenced their decision to work with a particular lender, compared to only 32% of Gen X and older respondents.

Both high-tech and high-touch experiences are in demand. Borrowers who utilized an online application appreciated the process because it was more straightforward (59%), faster (58%), and allowed them to apply at their own pace (56%).

More than half of survey respondents indicated that online options make the home buying process more accessible, with added convenience (52%) being the top reason. Speed (41%) and ease of use (37%) were also significant factors.

However, there is a strong demand for a balance between high-tech and high-touch experiences, particularly among Millennials, with 45% expecting their mortgage lender to work with them both digitally and in-person.

Most lenders offer high-tech options, and the majority of borrowers utilize them. In fact, 45% of borrowers were offered a mobile app by their lender and used it (an increase from 39% in 2022).

Sixty-five percent of borrowers were offered and used an online application by their most recent lender (up from 60% in 2022), while the majority of borrowers (65%) were offered and utilized an online portal to electronically upload documents.

Similarly, 65% of borrowers were offered and used an online portal for electronically signing and notarizing documents. Although 60% of borrowers found their recent mortgage experience easy, only 36% reported having a great online experience. However, this figure has improved from 2022, when only 33% of homeowners claimed that their lender offered a great online experience.

Borrowers’ expectations revolved around a simpler process, electronic document verification, and a safe and secure platform (48% each). The expectation that online offerings would result in lower costs and a quicker process was also important (46% each). Older borrowers were more likely than younger borrowers to expect lower overall costs as part of a great online experience (55% versus 38%, respectively).

Post-COVID, the importance of a human connection in mortgage lending has increased.

Borrowers and potential borrowers desire human https://sprintfunding.com/contact/, with 46% citing their preference to work directly with a person as the top reason for not filling out an online application (an increase from 39% in 2022).

Interestingly, older borrowers appear to be less interested in human https://sprintfunding.com/contact/. Fifty-one percent of older borrowers (Gen X and up) preferred the elimination of the need to meet in person through online applications, compared to only 31% of Gen Z and Millennial borrowers.

Experienced homebuyers place a higher importance on digital and online options. Specifically, those who have taken out five or more mortgages were more likely to interact with their lender through online tools, with traditional methods supporting the process, compared to less experienced borrowers (24% versus 14%).

They were also more likely to utilize online portals for uploading and signing/notarizing documents, with 71% utilizing each option compared to 63% among those with less mortgage experience.

Experienced borrowers also have high expectations for their online experience, including the ability to electronically verify documents (58% versus 45% for less experienced borrowers) and the flexibility to work digitally or with a person if they choose (49% versus 39%).

They were more likely to report a great online experience with their most recent lender, with 42% reporting a positive encounter compared to 34% of less seasoned borrowers.

Overall, it is important to tailor lending offerings to borrowers’ preferences and needs based on their individual mortgage experiences, particularly as borrowers have had different experiences depending on interest rates and borrowing during or after the pandemic.

People still value human connection in mortgage lending, especially after the COVID-19 pandemic. Many borrowers prefer to work with a person, as indicated by the top reason for not filling out an online application, which increased from 39% in 2022 to 46% in 2023.

However, experienced borrowers have different preferences and needs, which should be considered when offering mortgage services.

Interestingly, older borrowers seem less interested in human https://sprintfunding.com/contact/, with 51% of them liking the fact that online applications eliminate the need to meet in person. In contrast, only 31% of Gen Z and Millennial borrowers feel the same.

Experienced homebuyers consider digital and online options more important than less-experienced borrowers, with 31% versus 24% indicating that they prefer to interact with their lender through online tools, supported by traditional methods.

Specifically, experienced borrowers are more likely to use online portals for uploading and signing/notarizing documents, and they rate their online experiences with lenders higher than less-experienced borrowers.

Furthermore, most borrowers find the amount of https://sprintfunding.com/contact/ from their lenders to be just enough, with 79% saying that the outreach was for updates on the progress of the loan or requests for information or clarification.

However, over a quarter of Gen Z and Millennial borrowers and the most experienced borrowers feel that lenders https://sprintfunding.com/contact/ed them too much. High-interest rate buyers find the mortgage lending process easier from start to finish, and a significant number of recent borrowers think that online mortgage processes make it easier to get approved.

Nonetheless, traditional methods are still preferred by over two-thirds of high-interest rate borrowers. High-interest rate borrowers highly value relationships, which means they are likely to consider multiple lending institutions during the mortgage process.

In fact, most borrowers who recently went through the mortgage process considered two lending institutions before selecting a lender, but a third of them only considered one. Gen Z and Millennials are more likely to have considered two lending institutions than Gen X and older individuals who tend to consider only one.

Low-interest rate buyers’ digital preferences were shaped by the COVID pandemic during the lowest interest rate period one to two years ago. Those who used an online application during that time liked it because they didn’t have to meet in person. If they apply for a new mortgage, they would prefer their interactions with their lender to rely more on digital/online tools.

Low-interest rate buyers are less concerned about the characteristics of their lender, with lender transparency being the least important for those involved in the mortgage loan process one to two years ago. This group is also more cautious and likely to wait and see how the market plays out before selling their house compared to the most recent buyers.

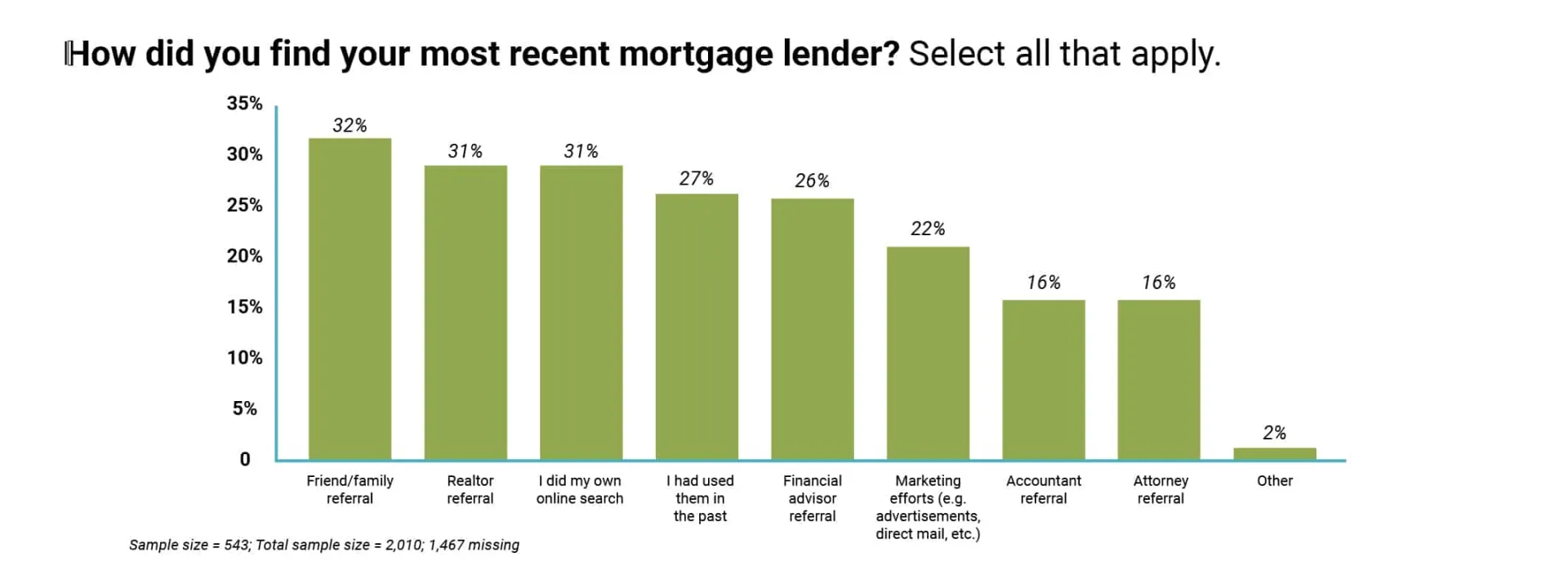

Borrowers, especially new and younger ones, rely on referrals from realtors, family members, and friends to choose a lender, highlighting the importance of strong relationships. For those who have only taken out one or two mortgages, a referral from their realtor is important when choosing a lender, with 24% considering it as one of the top three most crucial factors.

Referrals from family and friends were also popular, with 32% finding their most recent lender through them. Meanwhile, 31% relied on their realtor, and another 31% conducted their own online search. Gen Z and Millennials were more likely to have found their recent mortgage lender through a friend or family referral, at 40%.

When asked why their realtor referred to a specific lender, the majority of borrowers believed it was because of an existing relationship between the realtor and lender (53%), the lender’s extensive experience (43%), or helpful/knowledgeable customer service (43%).

Meanwhile, nearly one-third believed that their realtor referred the lender because of their good digital options and capabilities (32%).

Building Relationships for an Uncertain Future

The survey results paint a somewhat daunting picture. The environment is uncertain, the market may be stagnant, and the extent and duration of this are unclear. Borrower preferences are heavily influenced by demographics, recent experiences with interest rate volatility, and the pandemic.

As a lender, what should be your course of action?

Generalizations can only take us so far. Your understanding of your borrowers and local marketplace should be the primary factors shaping your strategy.

Here are some key steps:

■ Improve your offers: Even the oldest and least tech-savvy borrowers want and expect the convenience of digital portals and processes as part of your service portfolio.

■ Digitize your back office. Your technology investment should not be limited to customer-facing offerings. Intelligent back-office automation will free you and your team for the crucial task of maintaining relationships.

■ Cultivate relationships with realtors. Borrowers rely on referrals from realtors, friends, and family. Developing and sustaining relationships is vital – the quality of your referral network could make all the difference. Keep in mind that “high tech, high touch” is what nearly all borrowers desire and expect.

■ Understand your borrower. Recognizing borrowers’ preferences by age and experience will enable you to “meet them where they are.”

■ Maintain https://sprintfunding.com/contact/. While we’ve already discussed relationships, it’s worth emphasizing their long-term value. An ongoing relationship will generate repeat business and referrals in the years to come.

Lastly, be prepared for change. Five years ago, no one anticipated a global pandemic, inflation, or an interest rate surge. The home lending marketplace will undoubtedly change again in the next five years, or even sooner.

Whether the market maintains its current trajectory, or falling interest rates spark a refinancing boom, adopting the right technology and maintaining a human touch will ensure a steady and growing stream of business comes your way in an unpredictable future.