People will often find themselves asking which is a better low-down-payment mortgage: The Conventional or the FHA loan?

FHA loans accept credit scores that start at just 580, along with a 3.5% down payment, which makes them a great option for people with low-to-average credit.

However, insurance is always required with an FHA mortgage.

On the other hand, conventional loans are a better choice for people with good credit, or if you plan to stay in your home for many years. However, the hard part is reaching a credit score between mid to high 600s — but in return, you can get a conventional loan with a downpayment of just 3%. Moreover, you can also cancel mortgage insurance later.

We tackle everything you need to know about both FHA and conventional loans in this post.

We’ll also answer some frequently asked questions that people have when thinking about making their first home investment.

Conventional vs. FHA Loans

Today, there is a wide range of low-down-payment options available for buyers. However, many of us will still choose between an FHA loan with a 3.5% down payment or a conventional loan with a 3% down payment.

As a result, many people will often ask which option is better. The answer depends on your current situation.

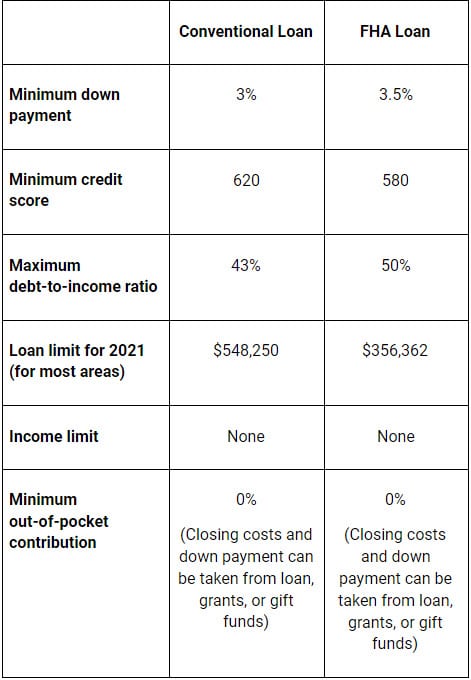

FHA vs Conventional Loan Comparison Chart 2021

Here’s a brief overview of what you need to know about qualifying for a conventional loan vs. an FHA loan.

Pros and Cons of FHA Loan vs Conventional

Below are a few differences between the two loans available to homebuyers, which highlight both the pros and cons of each option.

Credit Score Requirements

When trying to choose from a conventional or an FHA loan, know that your credit score matters. This is because it determines whether you’re eligible for the program and will also affect your mortgage payment.

The minimum credit score requirements for these options are:

- A score of 620 for conventional loans

- A score of 500 with a 10% down payment or a score of 580 with a 3.5% down payment for FHA loans.

As such, an FHA loan is the only option available for you if your credit score falls between 500 and 620.

But if you have a credit score over 620, you can get access to a conventional loan with just 3% for your down payment

Debt-to-Income Ratio

Another thing you need to consider is your “debt-to-income ratio”, which refers to the debt you have each month, against your monthly gross income.

Another thing you need to consider is your “debt-to-income ratio”, which refers to the debt you have each month, against your monthly gross income.

FHA loans allow for a more generous 50% maximum DTI, while conventional loans only permit you to have 43% DTI. This means that your debts shouldn’t go above 43% of your gross income.

Keep in mind though, that even with FHA loans, you’ll still need to shop around if you have a DTI of over 45% since it can become difficult to find lenders that offer more flexibility than this.

Debt-to-income ratios are more likely to make a difference in expensive areas such as major cities where there are higher housing prices.

If you plan to buy in places like New York, Seattle, or Los Angeles, your mortgage costs and monthly debt will take up a lot of your income. This is simply because houses in these areas are much more expensive.

As a result, getting an FHA loan with flexible standards is much better suited for you compared to a conventional plan.

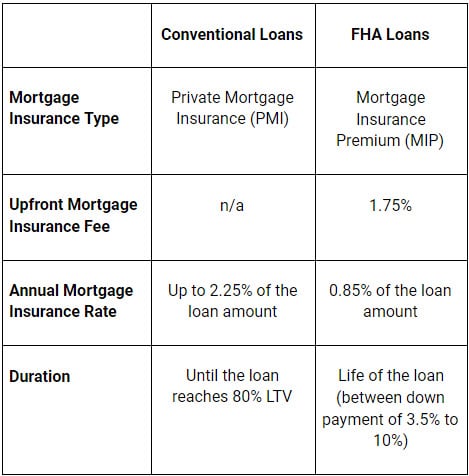

Mortgage Insurance

Conventional and FHA loans will both charge for mortgage insurance. However, their costs vary depending on the kind of loan you have and how long you’re planning to maintain the mortgage.

Below is a table that compares the two available options.

FHA mortgage insurance stays the same for every homebuyer, with a one-time upfront fee of 1.75% and 0.85% of the loan every year.

Conventional mortgage insurance, on the other hand, will vary depending on your loan-to-value ratio and credit score. In other words, the cheaper option for your needs will depend on your situation.

Moreover, a conventional mortgage will be removed once you’re at 80% loan-to-value.

This means that your conventional loan can get better value over time, and this is especially true if you’re a borrower with great credit scores. But it’s also good to consider any upfront charges.

FHA loans charge a different mortgage insurance premium at the closing time — this is known as Upfront MIP.

This cost is 1.75% of the loan you take; it is added to the balance and can’t be recovered except through the FHA Streamline Refinance. Meanwhile, a conventional loan doesn’t have any upfront fees for mortgage insurance and only charges by the month.

Mortgage Rates

Generally, an FHA loan will look lower than a conventional loan on paper. For example, this report has found that the average FHA rate is as low as 2.5%, while the conventional rate is at 3%. Unfortunately, these values can’t be trusted because they will likely be different from the average value.

Furthermore, credit scores and PMI may also affect mortgage payments and interest rates.

When it comes to conventional loans, a lower credit score will reflect higher interest rates. But if your score ranges from low to mid-600s and more, then an FHA loan could be a better choice.

Mortgage Payments

While your credit score gets higher, a conventional loan can become more useful; this is because your mortgage rate is dropping.

Because of this, PMI and monthly payments also drop. This is a lot different from the way that FHA loans work.

Using an FHA loan, however, the MIP cost and mortgage rate will stay the same, no matter how good or bad your FICO score is. This means that FHA loans are often the best choice for short-term loans.

For instance, a loan size that costs $250,000 paired with today’s mortgage rates will mean that FHA loans are 10% cheaper for borrowers with great credit scores. Even better is that borrowers with poor credit get loans that are 26% cheaper.

However, long-term borrowers who have above-average scores will likely find a conventional loan to be much more economical compared to FHA loans.

Keep in mind that mortgage insurance for conventional loans can be canceled once you reach a 20% loan-to-value ratio. But an FHA mortgage insurance will last for the whole term of the loan.

This means that a conventional loan might be a cheaper option if you plan to stay in your house long enough to reach 20% equity. Doing this is a good move, especially if you have a great credit score.

FHA vs conventional Q&A

Here are just a few of the most asked questions regarding these two home loan options. We’ve provided the answers here in a short and precise manner, so you don’t have to look for the answers above.

Which is a Better Loan: FHA or Conventional?

When trying to decide which option is better, consider your financial circumstances.

When trying to decide which option is better, consider your financial circumstances.

If you have a high level of debt (50% DTI or more) or have a credit score below 680, then an FHA loan might be better for you.

But if you have a higher credit score, then a conventional loan might be a more attractive choice since you can get lower monthly payments and interest rates.

Can Homeowners Switch Between Loans?

Yes, you can switch from an FHA to a conventional loan when you refinance your mortgage.

However, this means getting a new conventional loan to pay for the existing FHA loan.

This is a good move if you have a minimum of 20% equity on your home, along with a credit score of 620 or higher.

You might also be able to save when switching from an FHA to a conventional loan without PMI.

Are There Benefits to a Conventional Home Loan?

If you’re able to get a conventional loan with a down payment of 20% or more, then you won’t need to pay for mortgage insurance.

This is a huge benefit that FHA loans can’t provide since it will need mortgage insurance no matter how big your down payment is.

A conventional loan also lets you put a 3% down payment, while an FHA loan requires 3.5% as the bare minimum.

Moreover, conventional loans can provide you with lower mortgage rates if your credit scores are higher. This is excellent news if your credit score is 720 or more.

What Credit Score Do I Need for a Conventional Loan?

A conventional loan has a minimum credit score requirement of 620. However, some lenders may set their requirements and can be as much as 640, 660, or even higher.

Additionally, the conventional mortgage rate could be better if your credit score is higher. So if your credit is on the lower end, make sure to have a look around various lenders to find the best deal.

What Credit Score Do I Need for an FHA Loan?

An FHA loan will typically need a score of 580 or more in most cases. If you make a 10% or higher down payment, you could be eligible for an FHA loan even if your credit score is between 500-580.

However, you’ll need to look for the right lender, since not every mortgage company will provide deals like this.

What are the Conventional Loan Requirements?

You could qualify for a conventional loan if you meet the following criteria:

- You have a minimum credit score of 620

- Make a 3% down payment on the house

- Have a debt-to-income ratio of 43% or lower

- A steady, two-year employment history that you can prove with bank statements and tax returns

If you wish to qualify for a low-down-payment conventional loan, ensure that you purchase a single-family property (units of 2 or more are not allowed).

What are the FHA Loan Requirements?

You could qualify for an FHA loan if you meet the following criteria:

- Have a credit score of 580 or more

- A debt-to-income ratio lower than 50%

- Enough money to make a 3.5% down payment

- A steady income and job which you can prove with tax returns

You can also get an FHA loan with 1-, 2-, 3-, or 4-unit properties.

The Choice Comes Down to Your Circumstances

In the end, choosing the right loan for you comes down to your understanding of your financial needs and situation.

While an FHA loan has a less-restrictive set of qualifications and requirements compared to a conventional loan, it isn’t supported by a government agency.

An FHA loan is a safer choice in the long run since it is supported and insured by the Federal Housing Administration.

Moreover, you need to have a lower debt-to-income ratio, a higher credit score, and a down payment to get your hands on a conventional loan. There are specific loan limits for conventional and FHA loans; while you might need to pay mortgage insurance for conventional loans, you strictly need to pay a MIP for your FHA loan.

With so much to take into consideration, it’s best to weigh both pros and cons of these options carefully.

Be sure to take your qualifications into account so that you can make the next step towards a better future.

Want to know more about Sprint Funding loan options? Contact us today!