Say the words ‘The American Dream,’ and a few things come to mind in almost every American:

Democracy, rights, liberty, opportunity, and equality.

And although these aren’t things you can necessarily ‘touch’ – there are some physical items that most Americans still associate with living life the way it was always meant to be.

Having a house to call their own is one of them.

More than 7 in 10 Americans list buying a house as one of their New Year’s Resolutions each year – but much fewer than that actually achieve them.

Part of that is because there are always so many conflicting opinions about whether or not it’s the right time to buy…

Luckily, on this page, we’re here to help you answer two important questions:

- Is 2023 a good time to buy a house?

- How do I buy a home in 2023?

Let’s get started:

Is 2023 A Good Time To Buy A House?

Short Answer: Yes.

Of course, we’re sure you want to know our exact reasons for this – so read on to find out why now, more than ever, is the ideal time to buy your first or next home.

Why Buy Now?

Mortgage Rates Are DROPPING.

Let’s talk about interest rates – the scary part about buying a home.

After the release of December’s job report, 30-year fixed-rate mortgage rates fell 0.3%, the largest one-day rate drop in over a month.

With inflation pressures retreating, mortgage rates drop too.

In fact, they’ve been dropping at their fastest rate since 2008!

And what’s more, affordable homeownership policies out of Fannie Mae and Freddie Mac offer mortgage rate discounts for low and moderate-income first-time buyers!

As much as 1.75 percentage points off their interest rate!

Let’s find out more about those discounts:

Mortgage Rate Discounts For First-Time Buyers

Navigating the various different government programs and schemes available can often be overwhelming.

But now, eligible first-time buyers can get an automatic mortgage rate discount on conventional mortgage loans instantly – without having to get to grips with the various options on the market.

This is through the FHFA (Federal Housing Finance Agency) First-Time Home Buyer Mortgage Rate Discount program.

In short, it allows low to moderate-income first-time home buyers to purchase a primary home and finance it using a conventional mortgage – whether fixed-rate or adjustable-rate.

The program applies to single-family homes, which includes condos, townhomes, and 2-4 unit properties.

As we mentioned, discounts of up to 1.75 percentage points off interest rates are available.

However, this program is only temporary.

Once it’s gone, it’s gone.

Home Values Didn’t Crash In 2022

Against all odds, the home market didn’t crash last year.

Single-family homes, including detached houses, townhomes, and condos, dropped 4% in the first week of 2023, and home inventory is at its lowest in 6 months.

But demand for homes is still strong and set to climb.

With this in mind, a shrinking supply and rising demand will most likely push home values higher – meaning that now is a great time to buy to take full advantage.

Buyers Now Have The Upper Hand

Traditionally, sellers are the ones who can control negotiations.

Until very recently, conditions have been weighted in favor of sellers, who have been able to wait for potential buyers to meet their asking price or even bid more to secure a home.

Now, the tables have turned.

Sellers have lost their leverage and have to make more concessions to buyers to make the sale.

This includes money for home repairs, closing costs, or even lowering their listing price altogether.

Tax Advantages

There are a wide variety of positive tax implications that come as a result of buying a home.

Perhaps the most attractive: significant tax deductions:

- Mortgage Interest

Deduct the interest you pay on up to $750,000 of mortgage debt. However, the proceeds must be used to build, buy or improve your primary residence or second home.

- Real Estate Taxes

Deduct state and local property taxes in the year you pay them. This deduction is limited to $10,000 per year. You can either deduct state and local income taxes or state sales taxes, but not both.

- Medical-Related Home Improvements

Deduct home improvement costs that help you or your dependents who live with you to live on a day-to-basis. This includes widening doorways, installing ramps or lifts, lowering cabinets, and adding railings.

- Capital Gains Tax Exclusion

This exclusion means you don’t pay taxes on the first $250,000 profit from selling your home (or $500,000 if you’re married.) This lets you keep more of your money than you would keep from a capital gains deduction.

How Do I Buy A Home In 2023?

Simply Follow Our Roadmap!

Although buying a home isn’t necessarily a quick process, that doesn’t mean it has to be a painful one!

Luckily, our expert team of financial specialists has created a step-by-step roadmap to help you navigate the occasionally confusing world of mortgages and more.

From finding a home to signing your name on the dotted line – we’ve got you covered.

Check out our complete guide to buying a home in 2023 below:

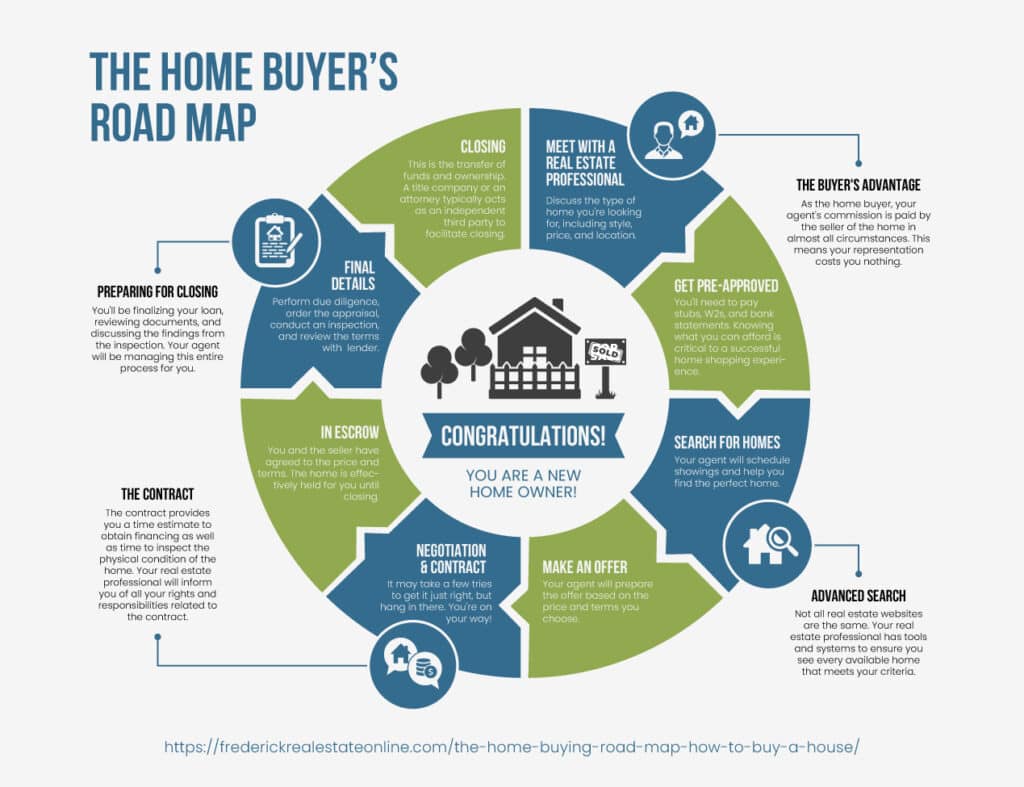

The Sprint Funding Home Buyer’s Road Map

- Decide To Buy A Home

Although this seems obvious, there are many things to consider when you start thinking about buying a home.

You need to be clear on what kind of home you wish to purchase, what’s negotiable for you, and what’s non-negotiable, whether that’s the number of rooms, the style of home, the location, and most importantly: your budget!

- Consult A Real Estate Expert

Share your findings with someone who knows the market like the back of their hand (such as our experts at Sprint Funding!)

The seller pays their commission in almost all circumstances, so your representation costs you nothing!

- Get Pre-Approved

It’s time to find out what you can afford. This way, you can think realistically and avoid disappointment as you start seriously searching for homes.

Provide a trusted local lender with pay stubs, W2s, and bank statements. Your real estate expert may even have some recommendations for you!

- Search For Homes

If you’ve done everything right up until this point, this should be the fun, stress-free part!

View as many homes as you have time for, and don’t be afraid to look for places that slightly exceed your budget – your agent may be able to help with that in the next steps…

- Make An Offer

Once you’ve found a home you like the look of, it’s time to put an offer on the table.

Your agent will help you craft an offer based on several factors, including market value, the property’s condition, contingencies, time frame, the seller’s motivations, and more so that both parties can feel like winners.

- Negotiate

A deal will rarely get accepted the first time around. But don’t panic!

Real estate agents negotiate for a living, so they’re experts at ensuring you get a fair offer for the home you’ve fallen in love with.

- Contract Signing

Once a deal is accepted, you’ll have time to inspect the home in more detail, and your real estate agent will advise you of your rights and responsibilities related to your contract.

At this point, the property is ‘in escrow’ – in other words, it’s held in your name until closing.

- Apply For Loans

Unfortunately, this means paperwork, but your real estate expert can help you make this part of the process as simple as possible.

Don’t rush, and take your time to do your due diligence.

- Inspections & Appraisals

Now, you can order an appraisal and conduct a full home inspection.

At this point, you’ll review the conditions of the house and see if it’s in line with the terms of your contract. Otherwise, further negotiations (and repairs) may be needed.

- Close The Deal

This is the final transfer of funds and ownership to you. After this step, the house will be officially yours!

A title company or attorney usually acts as an intermediary to facilitate the close, but your real estate expert can also help you with the paperwork.

And Just Like That – You’re Done!

See how simple things can be with Sprint Funding on your side?

If you’d like to find out more about how we can help you buy your first or next home, and offer you the best advice thanks to over 15 years of experience under our belts: